Most people fall into two camps when considering their protection needs in retirement:

1.“I don’t get the point of protection”.

2.“My retirement savings will cover all of my needs”.

I regularly find myself challenging both of these outlooks.

There’s a phrase gathering speed in the industry that refers to retirement as life 2.0. I like this concept as replacing the word retirement with ‘Life 2.0’, highlights that this is going to be a long and active part of our lives. Ultimately, it helps people to engage and take action. To enjoy retirement, you need to feel secure and know your objectives and goals are safe or “protected”. With that in mind, protection in retirement is a vital aspect of planning for “life 2.0”.

I planned my retirement…

People tend to focus their planning efforts on the lead up to retirement (and rightly so!). However, if 2020 has taught us anything, it’s that your plan can easily be knocked off course. The point here is that planning does not stop in retirement. People are living longer and that means your financial plan needs to be agile and able to develop over time.

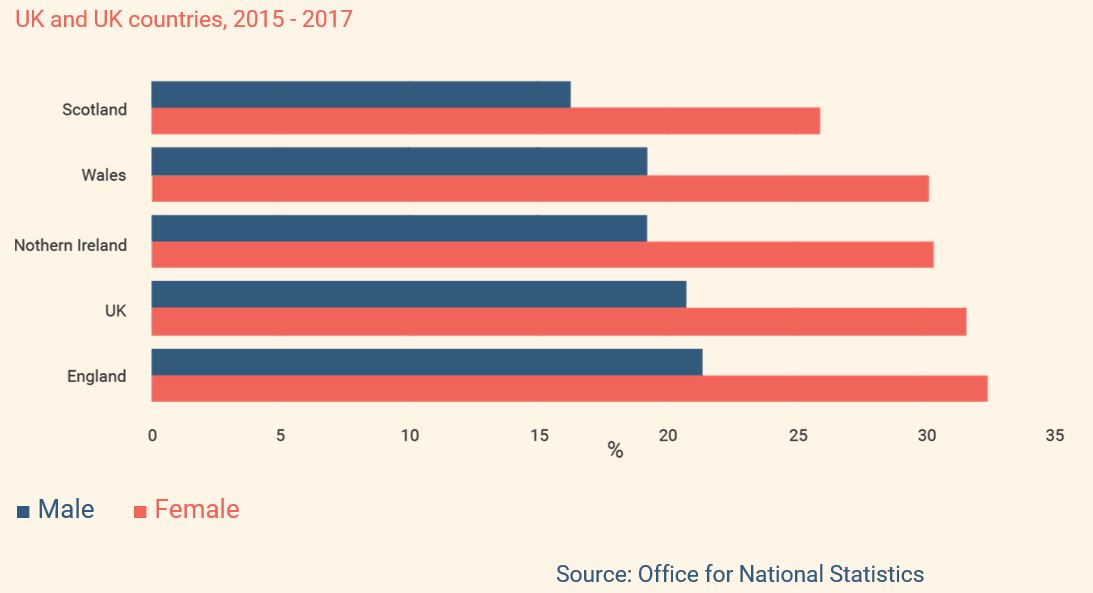

Chances of surviving to age 90, new-born males and females

UK Countries 2015-2017

It’s not just the shackles of the 09:00 -17:00 that you lose in retirement. You literally lose your largest asset: your earning power. Unfortunately, you also won’t have access to a crystal ball to know precisely how long your retirement funds will need to support you.

Average UK earnings last year were £31,461. Over someone’s typical working life (increased with inflation), that’s an asset of more than £2.2 million. In retirement, your income is provided for by either a final salary pension or an invested pot. So why wouldn’t you want to protect this in the same fashion? God forbid that retirement plan you have been working towards is knocked off course.

Protecting your retirement income

If you are approaching retirement, or have already stopped working, you might be one of the lucky few with an old defined benefit pension scheme. These are fantastic as they provide a level of guaranteed income. The sacrifice for this safety blanket, however, is typically the flexibility of death benefits and income options.

The unpleasant truth with these arrangements is that you and the pension provider are both gambling on how long you might live. This is exactly the same for annuities. As soon as we started talking about protection, it was always going to be a bit morbid – what would happen if you were to pass away earlier than expected and your spouse was reliant on your guaranteed income? Sometimes the income will only continue for a short period and, more often than not, it will be reduced to 50%. Many new clients have even come to me in real difficulty after realising they are not going to receive any death benefits at all.

So, how can you protect yourself, or your spouse, from having your income slashed or falling away entirely?

It depends on individual circumstances, but Family Income Benefit (FIB) is often a really nice option. FIB essentially guarantees regular income payments following death. Your guaranteed income can, therefore, continue without disruption. Not only that, but it can increase with inflation.

Take school fees, for example, a very common planning objective that you may relate to. At this stage of life, it will probably be for the grandkids, but if you were relying on your partner’s pension income to meet this objective and it disappeared, then you may have wished you protected it. FIB would allow you to cover the goal for the early period of your retirement whilst it is still applicable and continue to meet it should the worst happen.

Watch our webinar

Protecting your most important assetIn conversation with Jack Munday and Jordan Gillies

There are multiple “bolt on’s” that you can have with FIB, such as critical illness cover, which can also help for house renovations or simply ticking off some of the things on your bucket list. As with all protection, there is a time and a place for FIB. Some of the FIB products out there can be a tad restrictive on illnesses in later life (mainly after state retirement age) but can be a vital planning tool for those of you who planned well enough for early retirement.

Inheritance tax and your home (IHT)

Most people with a reasonably sized home and multiple investment pots, for a well-planned retirement, will typically find they are somewhat exposed to an Inheritance Tax (IHT) liability. If this is the case, the most useful form of protection in retirement will likely be a whole of life policy to cover you against inheritance tax liabilities.

Let’s have a look at it in action, with a client I recently dealt with:

This client has an estate valued at £1,312,500 which was made up primarily of his house, worth £850,000, and the remainder in a stocks & shares ISA and cash. Just like I did for him, I have broken down the IHT liability for you below:

| Whole of life – £325,000 sum assured | £850,000 |

| ISA | £262,500 |

| Cash | £50,000 |

| Total | £1,312,500 |

| IHT nil rate band | (£325,000) |

| Residence nil rate band | (£175,000) |

| Estate liable to tax | £812,500 |

| IHT due at 40% | £325,000 |

What a whole of life policy can do is allow him to cover that liability of £325,000 for his beneficiaries. If the premiums are up to date, a whole of life policy will quite literally pay out the agreed sum assured upon death.

To take it a step further, we established the policy under a trust, which meant his children were the beneficiaries of this policy. As a result, it will pay out to them directly and not get drawn into the estate upon distribution – a vital step!

Do you need cover to protect against illness or death?

Our advisers can give you the peace of mind that you and your family are protected against the financial consequences of the unexpected. Get in touch to discuss how we can help you.

The lovely 40% IHT charge can cause many people to wince purely as a point of principle. For others, it’s not a concern, as they feel that their beneficiaries will still get something and that’s good enough for them. I can sympathise with both sides of the argument and this is why peoples’ individual objectives are important.

According to HMRC’s most recent Inheritance Tax Statistics paper “Around half of the value of taxpaying estates held by those aged under 65 at death is made up by their main UK residence”.

You may have noticed that, in my example, the client doesn’t have enough cash in his estate to cover the IHT liability without the beneficiaries selling the home. However, it was the family home and he wanted it to stay that way. The policy was consequently extremely important for delivering this goal.

Sometimes, it’s not just about the money or the tax; there can be very personal and sentimental planning needs too. How do you feel about having to sell your family home?

Now, my whole of life example is very much the textbook option to cover yourself from an IHT liability of this nature. I have, however, repeatedly said that it’s all about the individual circumstances and objectives, so the correct solution is likely very specific to your situation.

This style of planning can often take the form of multiple 7-year cycles, for example, to remove assets from the estate. Depending on your age, it can be a lot more proactive and cost-effective to cover this short-term liability:

| Whole of life – £325,000 sum assured | 7 year fixed term – £325,000 sum assured |

|---|---|

| House | Normal |

| ISA | Normal |

Source: Lifequote – 21/04/2021

This is based on someone aged 67, so potentially at the start of their retirement, but the message is clear: by viewing your planning objectives in conjunction with any protection needs, you will save money and be considerably more financially agile, as you’ll have a plan to absorb any bumps along the road.

It doesn’t always go to plan

The critical illness market in retirement can be tricky to navigate and, if I’m honest, will rarely be appropriate. Most policies will have maximum ages at outset and (hidden away in the fine print) you may find that most illnesses are only covered up to age 60. So, why am I even talking about it? Because as I keep saying it’s all about the individual circumstance. There are providers out there that do solid critical illness plans for later life protection and it is still something to factor into your objectives – make sure every avenue is considered.

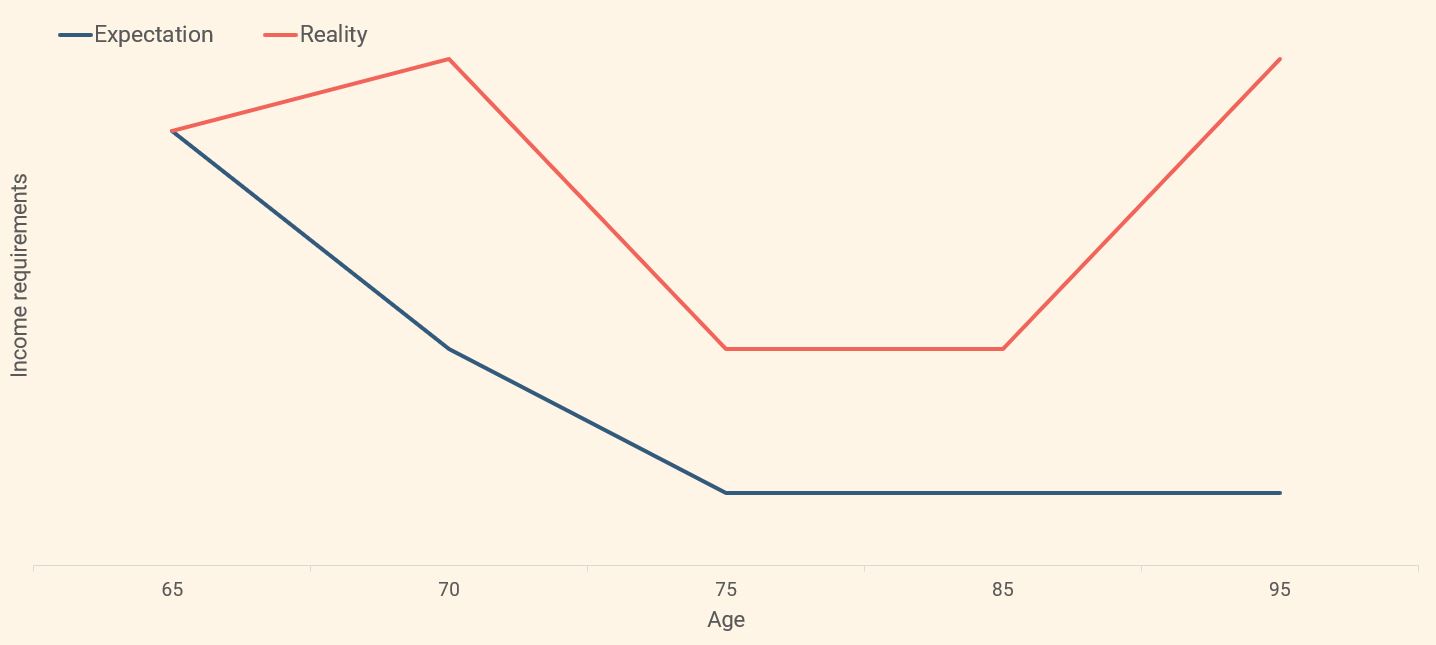

There is a common perception that our spending will gently decrease in retirement as we enjoy a slower pace of life. With modern medicine and a healthier lifestyle, however, you often see the opposite.

The graph below shows the reality of retirement spending patterns – as you have more time, you will spend more, not less! Yes, it will then slow down, but around the corner is the unfortunate truth of later life care costs.

How much do you need to retire and more…

How much income do you need to be comfortable, how much do you need invested and how to pay less tax...

That steep incline of the red line may well not occur but, with people over 60 being 10 times more likely to develop a chronic disease, there are some reasonably high odds that later life care costs will be needed. Pensions are fantastic vehicles for both accumulating wealth and providing sustainable income in retirement. However, you can back yourself into a corner financially if you suddenly need to draw say £100,000 for house renovations due to a severe illness – it could all be taxable, you could lose your personal allowance and your income stream will take a heavy hit.

A critical illness plan, if suitable, could pay-out on diagnosis and give you the safety net to renovate your home, support private medical treatment, reduce liabilities and more.

It’s not really about insurance

Protection is not about just holding insurance policies that you resent paying for seemingly no reward. Life 2.0 is about the peace of mind that your objectives are secure, as these don’t simply go away in retirement. People’s objectives both financially and in life, are such an individual and emotive thing. There’s not going to be a one size fits all solution and, if I’m honest, there may even be times where there isn’t a solution. This is fine as long as long as you are aware of it so it doesn’t come as a surprise.

Do you need cover to protect against illness or death?

Our advisers can give you the peace of mind that you and your family are protected against the financial consequences of the unexpected. Get in touch to discuss how we can help you.

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.

Saltus Financial Planning Ltd is authorised and regulated by the Financial Conduct Authority. Information is correct to the best of our understanding as at the date of publication. Nothing within this content is intended as, or can be relied upon, as financial advice. Capital is at risk. You may get back less than you invested. Tax rules may change and the value of tax reliefs depends on your individual circumstances.

About Saltus?

Find out more about our award-winning wealth management services…

Winner

Best Wealth Manager

Winner

Investment Performance: Cautious Portfolios

Winner

Top 100 Fund Selectors 2024

Winner

Best Places to Work 2024

£8bn+

assets under advice

20

years working with clients

350+

employees

97%

client retention rate